This formulation is nice because we can interpret the \(\beta\) coefficients as the change in the log-odds of the outcome for a one unit increase in the corresponding feature.

However other choices are available e.g. using a probit model where we use the cumulative distribution function of the standard normal distribution instead of the logistic function.

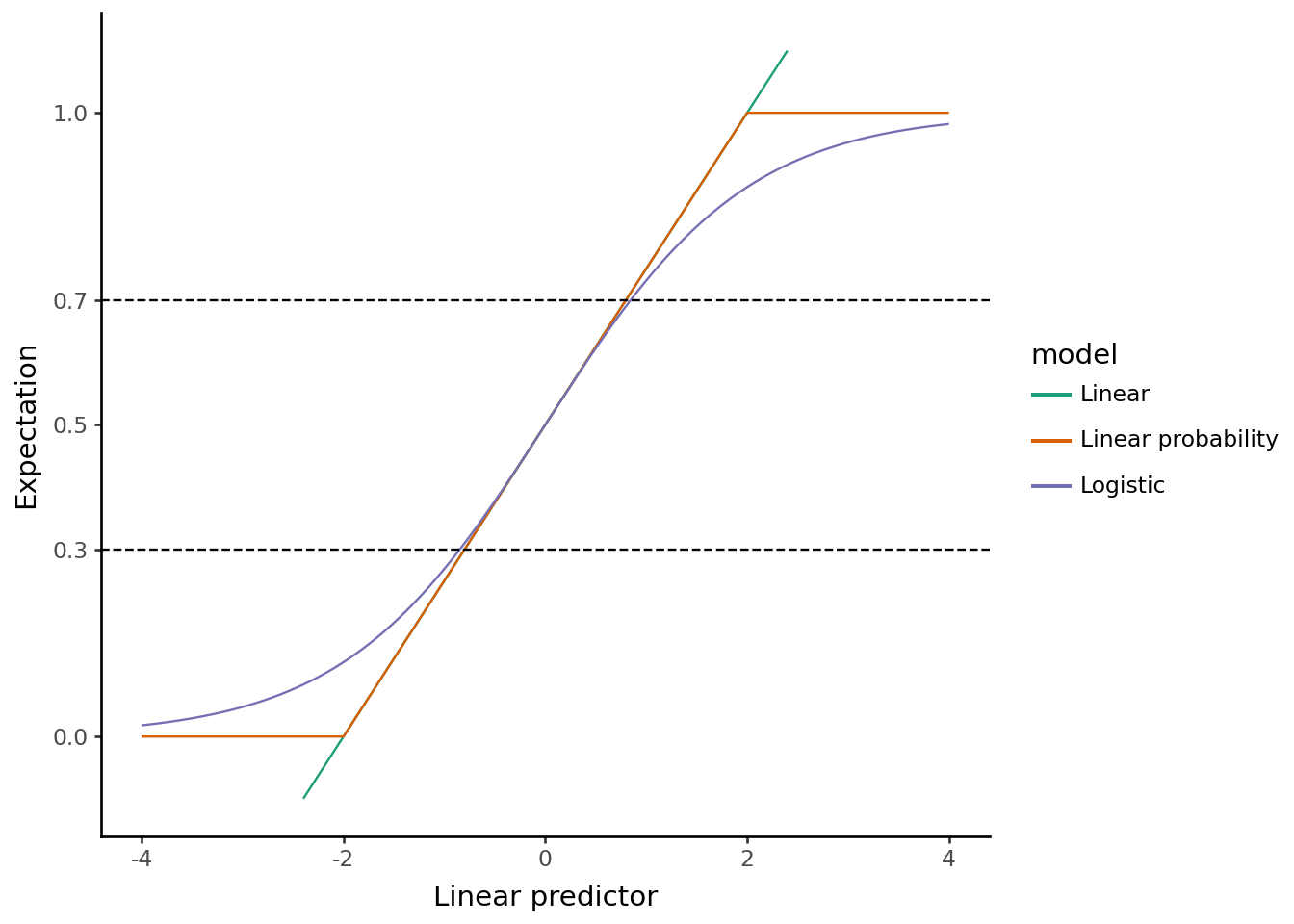

You can even use a gaussian GLM where we don’t transform the linear combination of the features at all.

TipPros and Cons of the linear probability model

The gaussian GLM has the benefit that the coefficients are interpretable on the probability scale directly and it has a (fast to compute) closed form solution.

It also turns out to be unbiased and consistent for the average marginal effect.

However, it can predict probabilities outside of \((0,1)\), so it is only a good approximation for the conditional expectation when the probabilities are between 0.3 and 0.7:

So we have a map between the linear combination of the features (\(X\beta\)) and the probability of the outcome \(p\), but we still need to specify the distribution of the outcomes to get a full generative model.

Given we have outcomes \(y \in \{0,1\}\), and assuming a conditional (on \(x\)) mean \(p\), the maximum entropy distribution is the Bernoulli distribution \[P(y) = p^y (1-p)^{1-y}\]

It’s more succinct, and you also get standard errors (and p-values), however the JAX implementation is more flexible. For example we could easily switch to a probit model by just changing the sigmoid function to the CDF of the standard normal distribution:

def predict_probit(weights, bias, predictors):""" Probabilities of the positive class """return norm.cdf(jnp.dot(predictors, weights) + bias)

While we used standard gradient descent above, with Flax we can use more sophisticated optimisers like Adam which adjust the learning rate for example using momentum.

import flax.linen as nnfrom flax.training import train_stateimport optaxclass LogisticRegression(nn.Module):@nn.compactdef__call__(self, x):# A simple linear layer with 1 output (the logit)return nn.Dense(features=1, use_bias=True)(x)def loss_fn(params, apply_fn, X, y): logits = apply_fn({'params': params}, X).squeeze()return optax.sigmoid_binary_cross_entropy(logits, y).mean()@jax.jitdef train_step_adam(state, X, y): loss_val, grads = jax.value_and_grad(loss_fn)(state.params, state.apply_fn, X, y) updates, new_opt_state = state.tx.update(grads, state.opt_state, state.params) new_params = optax.apply_updates(state.params, updates)return state.replace(params=new_params, opt_state=new_opt_state), loss_valdef train_model(X, y, key): model = LogisticRegression() variables = model.init(key, jnp.ones((1, 2))) tx_adam = optax.adam(learning_rate=0.1) state_adam = train_state.TrainState.create( apply_fn=model.apply, params=variables['params'], tx=tx_adam )for i inrange(101): state_adam, loss = train_step_adam(state_adam, X, y)if i %10==0:print(f"Epoch {i}: Loss = {loss:.4f}")print("Learned Weights: ")print(state_adam.params)train_model(X, y, key)print(f"\nTrue Weights: {true_w}")print(f"True Bias: {true_b}")

Epoch 0: Loss = 1.2306

Epoch 10: Loss = 0.7032

Epoch 20: Loss = 0.5401

Epoch 30: Loss = 0.4987

Epoch 40: Loss = 0.4956

Epoch 50: Loss = 0.4960

Epoch 60: Loss = 0.4958

Epoch 70: Loss = 0.4955

Epoch 80: Loss = 0.4951

Epoch 90: Loss = 0.4950

Epoch 100: Loss = 0.4950

Learned Weights:

{'Dense_0': {'bias': Array([0.30004427], dtype=float32), 'kernel': Array([[ 1.5121937],

[-0.8052652]], dtype=float32)}}

True Weights: [ 1.5 -0.8]

True Bias: 0.3

We can also use LBFG-S, which is a second order optimiser (it uses the Hessian - the matrix of second derivatives). So while each update is more expensive, it doesn’t require as many iterations:

@jax.jitdef train_step_lbfgs(state, X, y): loss_val, grads = jax.value_and_grad(loss_fn)(state.params, state.apply_fn, X, y)# L-BFGS needs value and grad passed to update updates, new_opt_state = state.tx.update( grads, state.opt_state, state.params, value=loss_val, grad=grads, value_fn=lambda p: loss_fn(p, state.apply_fn, X, y) ) new_params = optax.apply_updates(state.params, updates)return state.replace(params=new_params, opt_state=new_opt_state), loss_valdef train_model_lbfgs(X, y, key): model = LogisticRegression() variables = model.init(key, jnp.ones((1, 2))) tx_lbfgs = optax.lbfgs(memory_size=10) state_lbfgs = train_state.TrainState.create( apply_fn=model.apply, params=variables['params'], tx=tx_lbfgs )for i inrange(6): state_lbfgs, loss = train_step_lbfgs(state_lbfgs, X, y)print(f"Epoch {i}: Loss = {loss:.4f}") print("Learnt weights:")print(state_lbfgs.params)train_model_lbfgs(X, y, key)print(f"\nTrue Weights: {true_w}")print(f"True Bias: {true_b}")

Epoch 0: Loss = 1.2306

Epoch 1: Loss = 0.9719

Epoch 2: Loss = 0.5134

Epoch 3: Loss = 0.5010

Epoch 4: Loss = 0.4954

Epoch 5: Loss = 0.4950

Learnt weights:

{'Dense_0': {'bias': Array([0.30116275], dtype=float32), 'kernel': Array([[ 1.5125961],

[-0.8026858]], dtype=float32)}}

True Weights: [ 1.5 -0.8]

True Bias: 0.3

The real power here comes from the flexibility to train almost arbitrary models. A logistic regression is just a single layer neural network, but we can easily add more layers:

class LogisticRegressionNN(nn.Module):@nn.compactdef__call__(self, x):# A simple neural network with 1 hidden layer and 1 output (the logit) x = nn.Dense(features=10, use_bias=True)(x) x = nn.relu(x)return nn.Dense(features=1, use_bias=True)(x)def train_model_nn(X, y, key): model = LogisticRegressionNN() variables = model.init(key, jnp.ones((1, 2))) tx_adam = optax.adam(learning_rate=0.1) state_adam = train_state.TrainState.create( apply_fn=model.apply, params=variables['params'], tx=tx_adam )for i inrange(101): state_adam, loss = train_step_adam(state_adam, X, y)if i %10==0:print(f"Epoch {i}: Loss = {loss:.4f}")train_model_nn(X, y, key)

Epoch 0: Loss = 0.6905

Epoch 10: Loss = 0.5051

Epoch 20: Loss = 0.4985

Epoch 30: Loss = 0.4972

Epoch 40: Loss = 0.4964

Epoch 50: Loss = 0.4956

Epoch 60: Loss = 0.4952

Epoch 70: Loss = 0.4951

Epoch 80: Loss = 0.4950

Epoch 90: Loss = 0.4950

Epoch 100: Loss = 0.4950

While in this case we generated data from the logistic model so we don’t improve much on the loss. For more complicated data generating processes this general model training procedure is quite powerful.